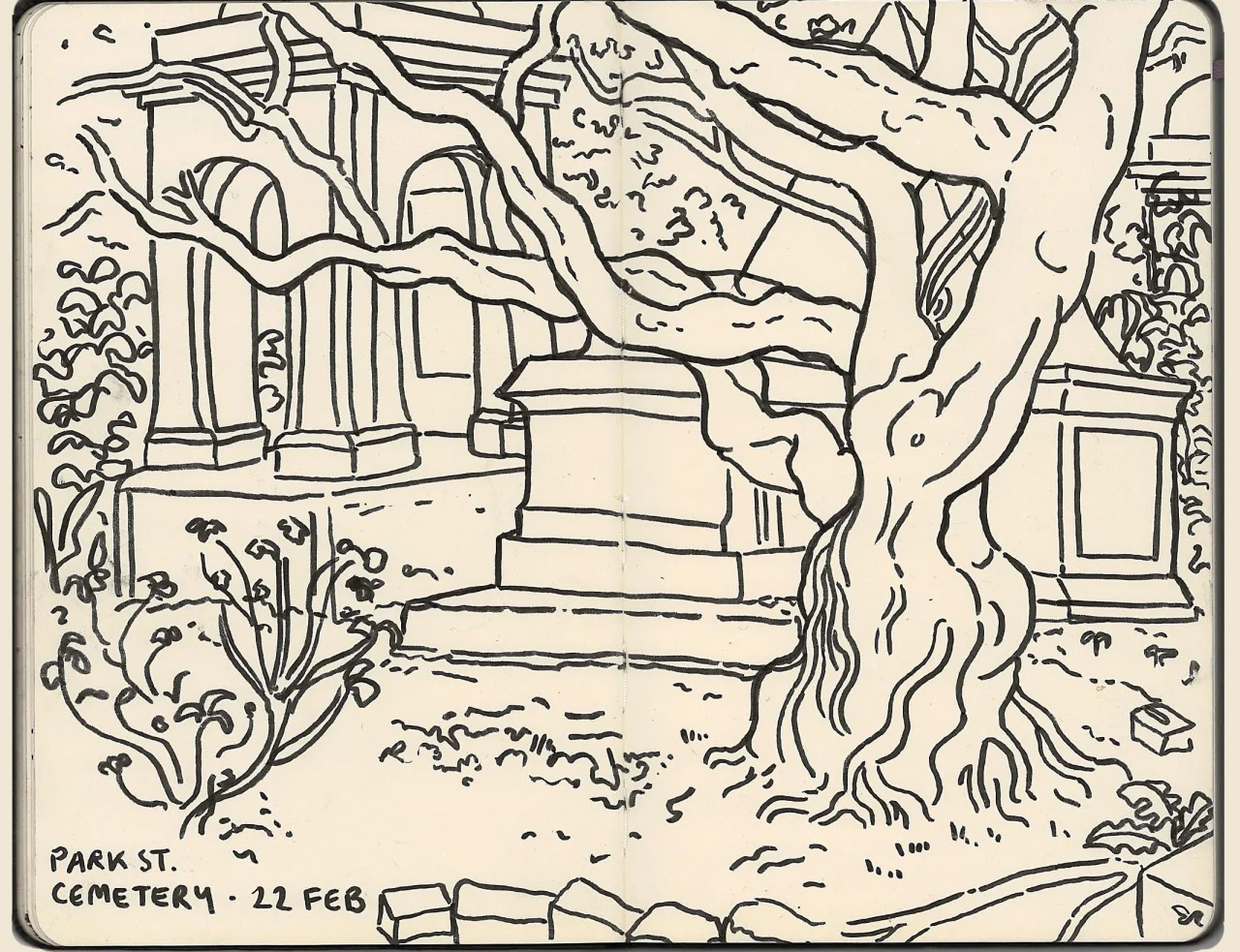

Hands-down my favourite, and the most peaceful place in Calcutta is Park Street Cemetery. An oasis of green rebelliously persevering in the face of all the traffic, dust and pollution of the city. When the Britishers first arrived in India they were dropping like flies from various horrible tropical diseases. Calcutta - being the colonial capital of the day - is now the final resting place to many ill-fated, 18th century noble men, women and children, almost all under the age of 40. The cemetery itself is a reminder of the original topography of the city; tropical jungle overflowing onto icons of the old British gentry. It’s a lost Louis’ Kingdom in the midst of dust, horns and madness.

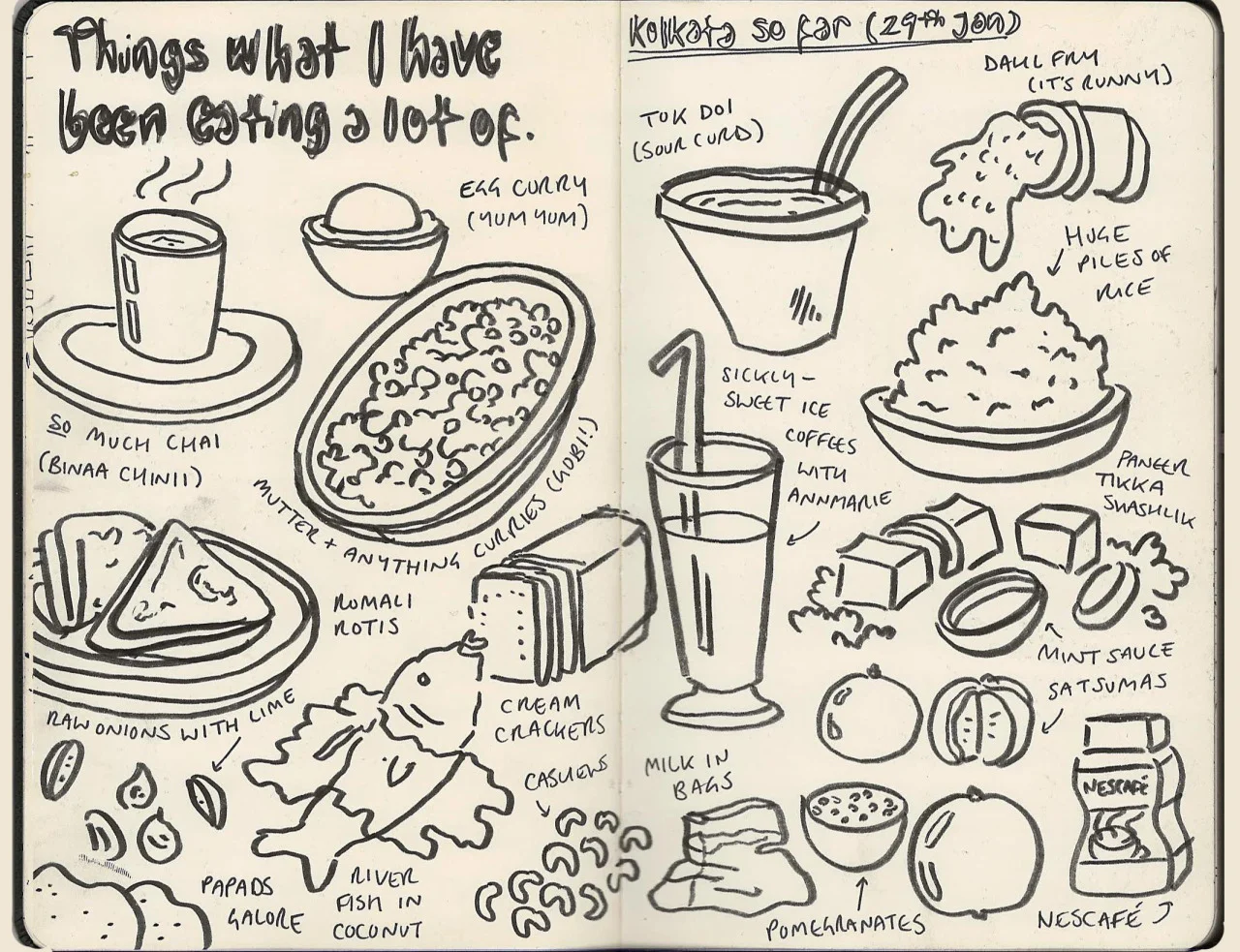

It took me three frickin weeks after arriving in India to get around to eating a masala dosa. When I did - it was more satisfying for the fact it cost the equivalent of 40p from a street-side shack near the Hope HQ in Lake Gardens. Fermented rice pancakes have never tasted so good.

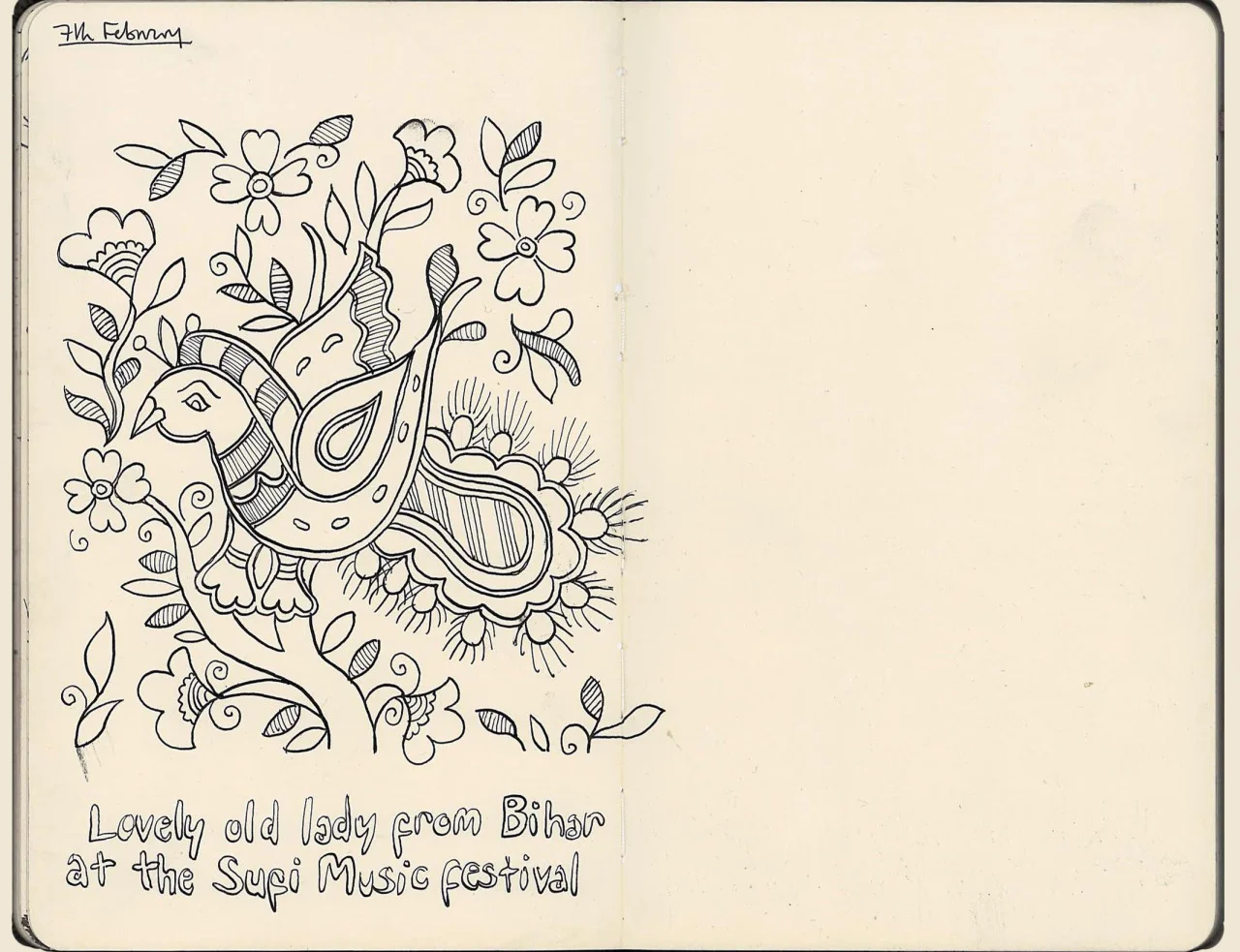

We went to a Sufi music festival and met an old lady selling hand-painted postcards from Bihar.

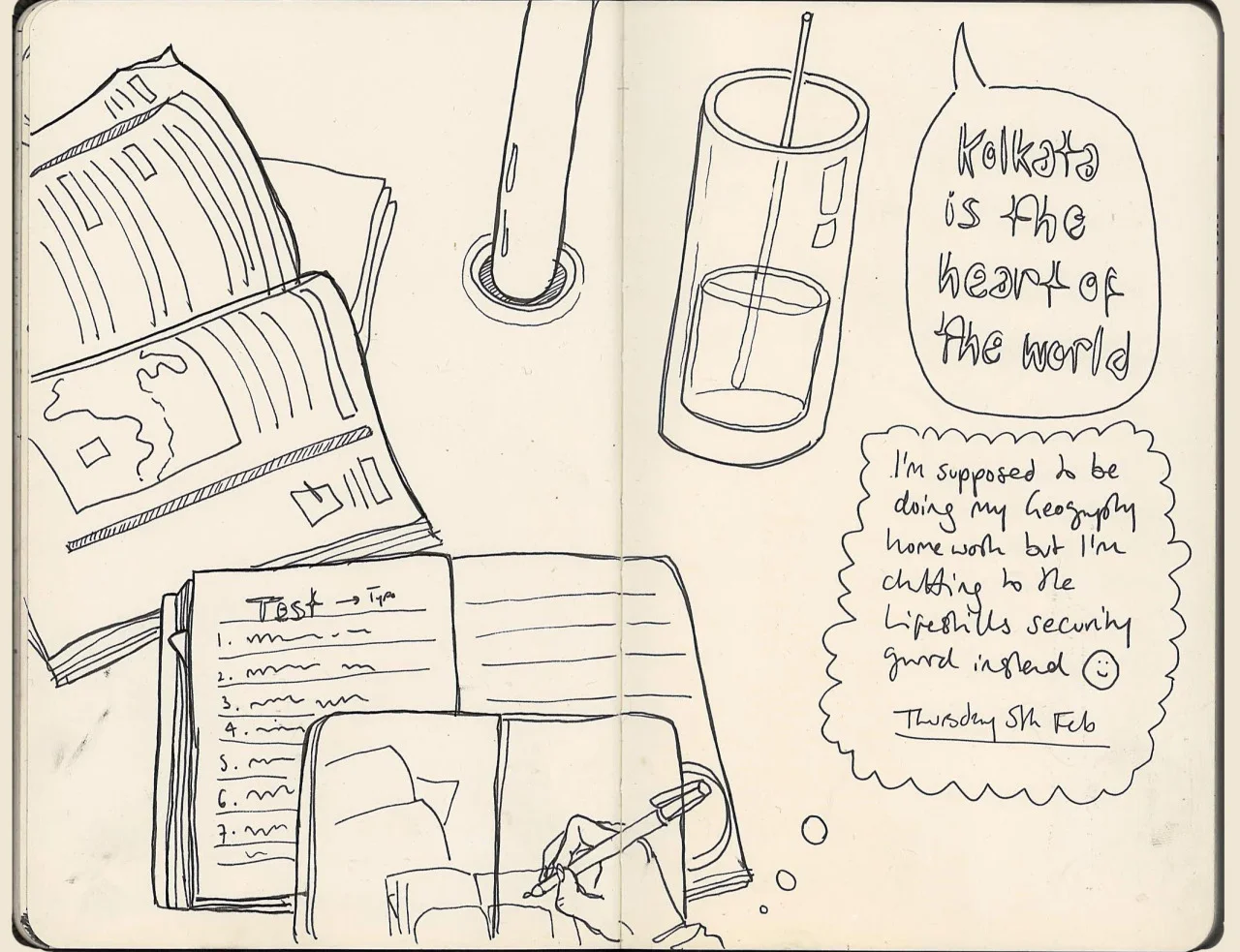

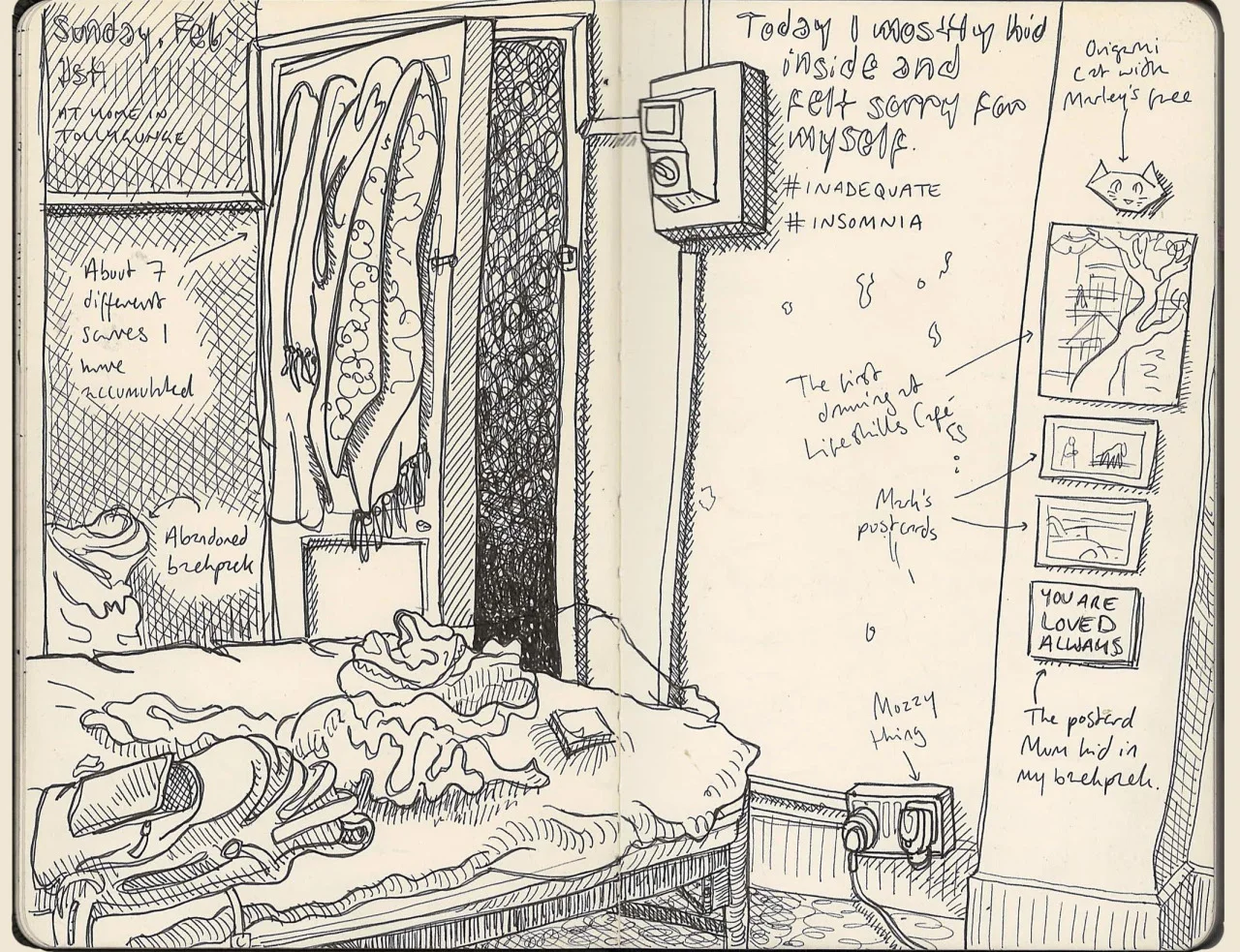

Every Tuesday and Thursday after my Indian social sciences lesson with the older girls at Hope Girls’ Home, I wander down to the Hope Lifeskills Café for chai and revision for the next class (I’m usually ever only a couple of chapters ahead of them - ssssh!). More often than not, I actually get bugger-all done because a friend or friendly stranger ambles past in search of a chat. Bengalis are genuinely the most chilled, friendly people… this day, I get talking to Hope’s security guy who tells me all about his daughter’s school successes, and his undying love for Calcutta

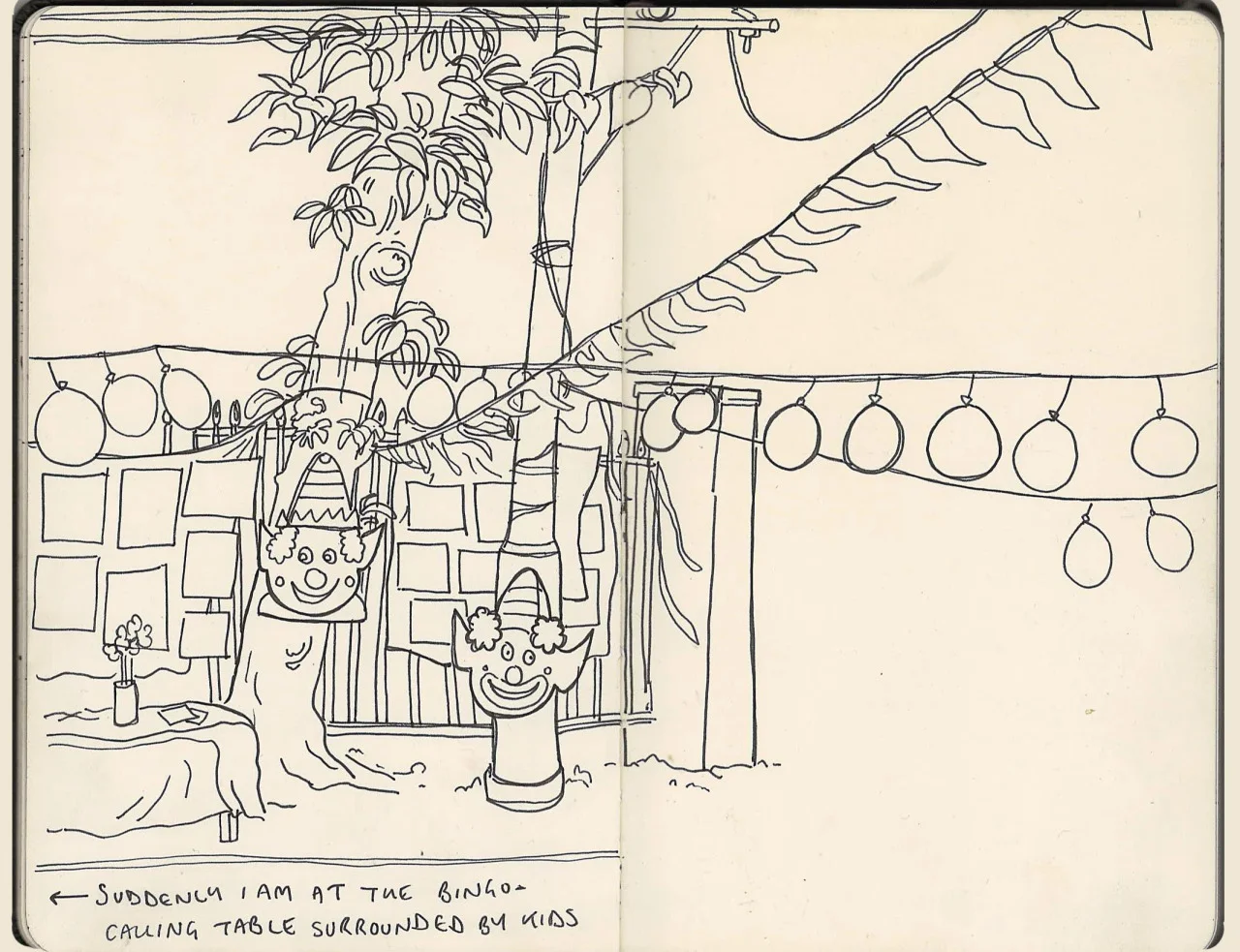

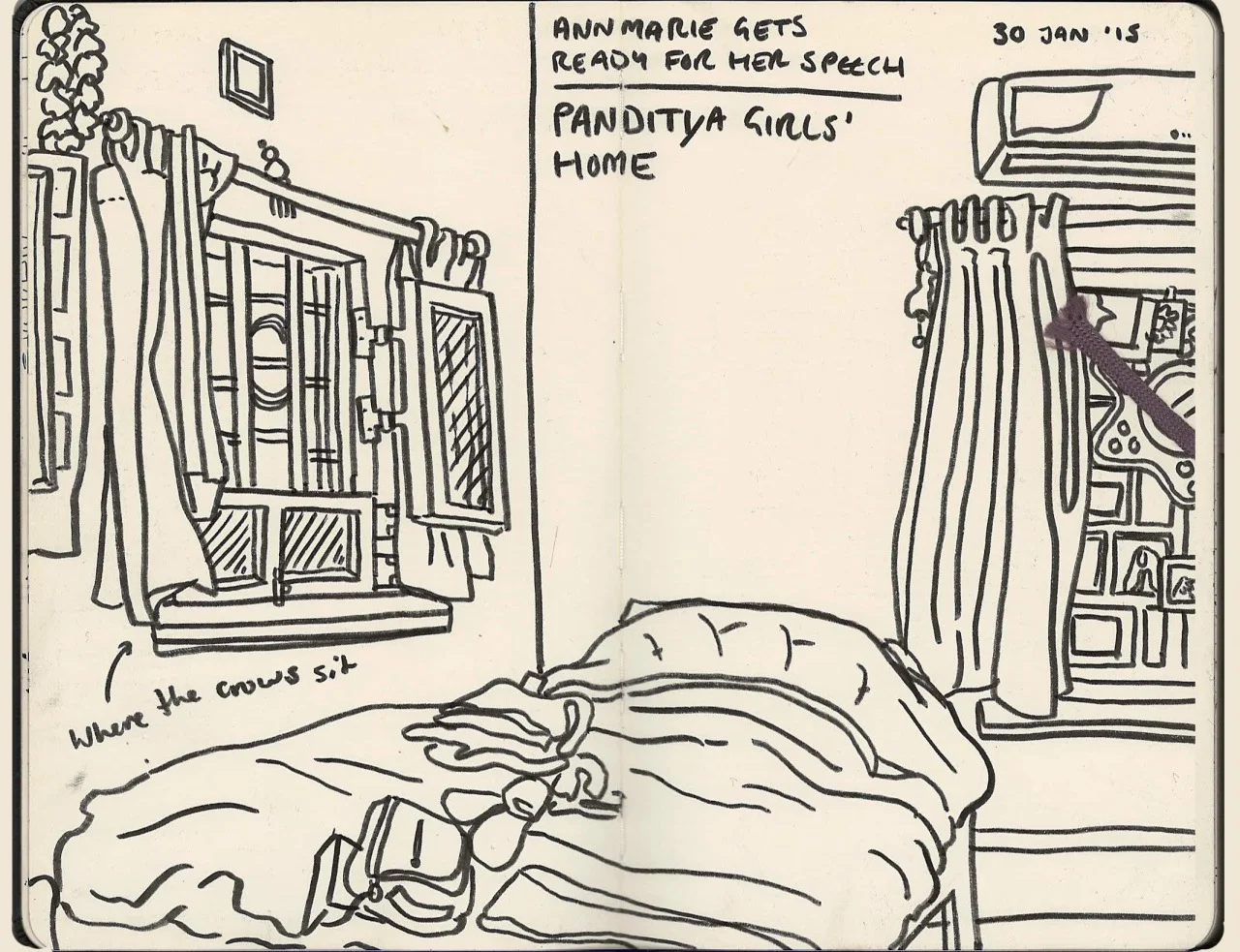

Attempting to remain inconspicuous as the PWB guys did their fire-twirling thing at the annual Panditya Street Carnival thrown by the girls at Hope Home for Girls. Sat quietly at a table outside Lifeskills Cafe, a lady with a bag of bingo tokens and a microphone from the late 1980s positions herself next to me. Suddenly, she begins barking orders at the crowds of children in extremely loud Bengali which is made much louder by the previously unseen amplifier which is turned up to 11, beneath my table. Now- instead of finishing my drawing in peace I am at the centre of the most raucous and confusing game of bingo ever seen, and it totally ruins the circus show. Oops.

In Calcutta, sometimes beer happens. And when it does, it is generally at the Fairlawn Hotel on Sudder street - just about the only place in Calcutta that could pass for being a ‘backpacker district’. I once nearly got thrown out of here for playing a game of shit head. Apparently playing cards are strictly taboo in this part of the world. The clientele is almost 100% NGO staff or MEN (the collective noun for males in india should always be in all-caps). Also, the only edible thing on the menu is fish and chips - and you’ll be lucky if they haven’t run out of that.

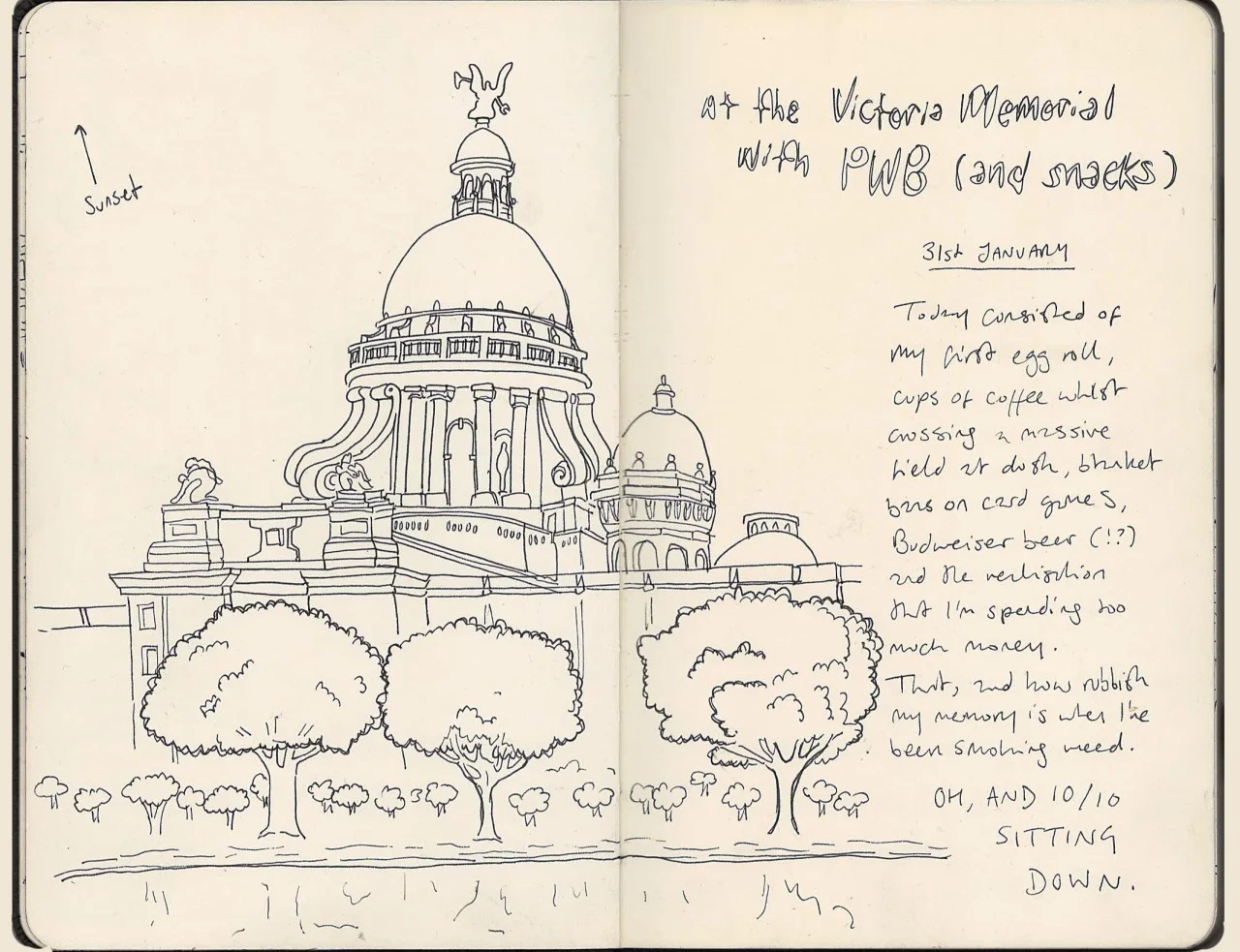

Today, I hung out with some of the overly-coordinated chaps from performers without borders. We ate an audacious amount of street snacks before paying the obscene (Rs150) fee to get into the Victoria Memorial. We spent most of our time there slating the Bastard Colonials (”Victoria, you slag”) and having a throughly satisfying sit-down on GRASS that was actually GREEN. Good day.

A bright, airy room on the top floor of the Hope Foundation’s Home for Girls is the home to Annmarie, a Hope Foundation employee, and all-around inspiring person. She spends six months of every year in Calcutta overseeing the dozens of projects and coordinating volunteers. She is also a bio-chemist and nurse. I’ve been hanging about her like a lost love-sick puppy since landing. (massive girl crush)

OMFG. Calcutta has amazing food. Bengali has just topped my chart of regional Indian dishes. They put rose water in their lassis and it’s just about the best god dayum thing in the world. Also huge props to the Hope Foundation Cafe’s fish thali - a steal at 60rups

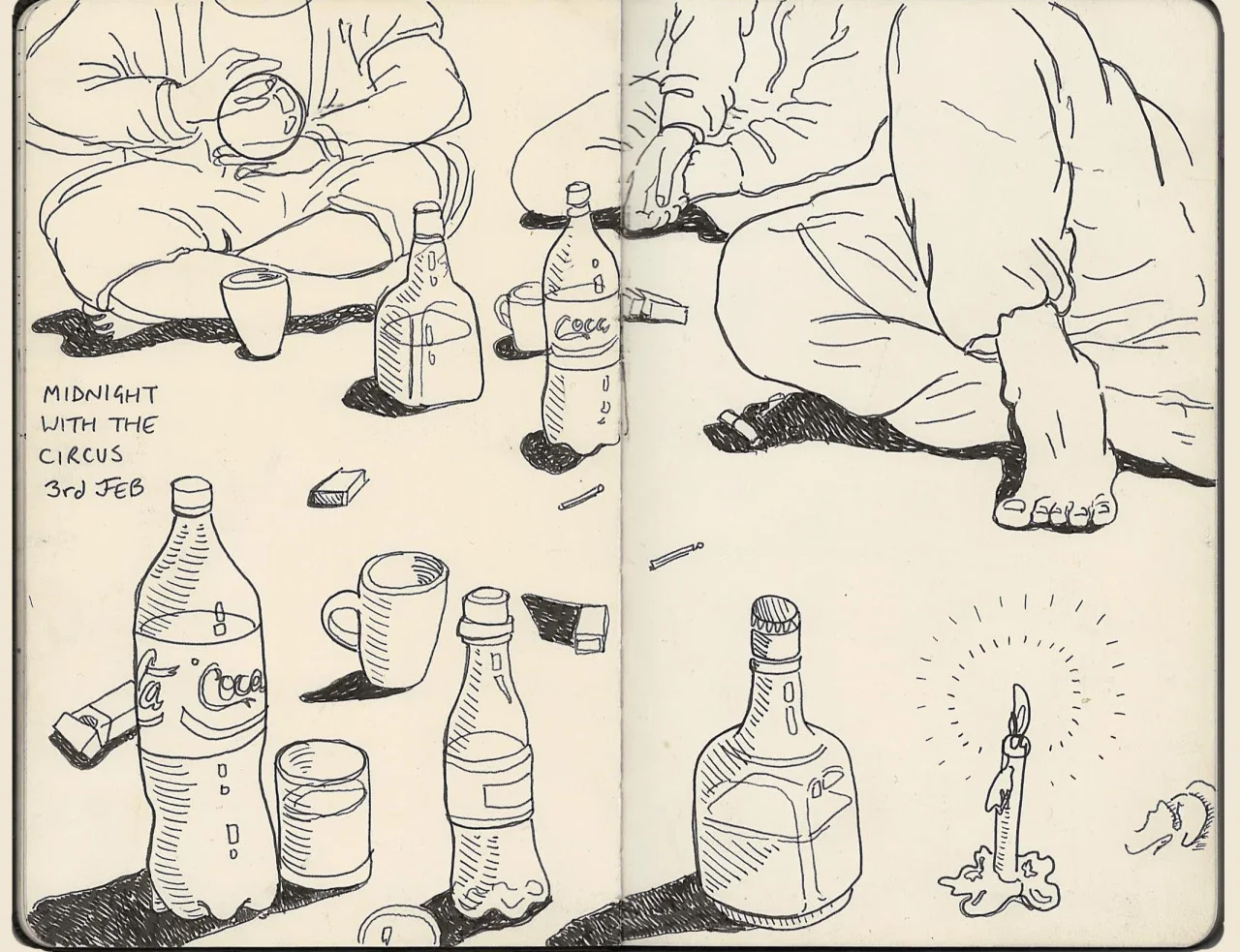

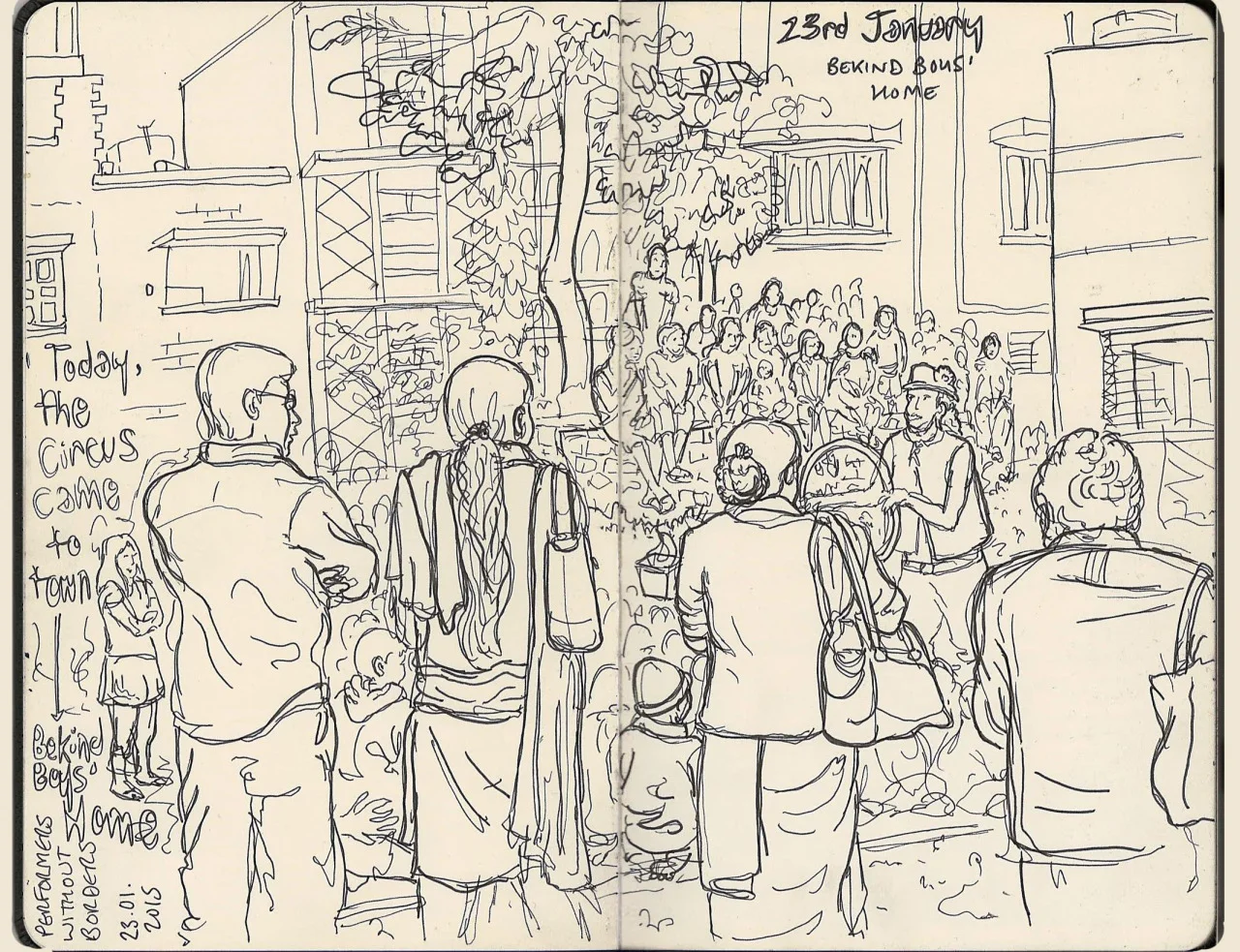

Performers Without Borders brought the circus to Bekind Boys’ Home, and basically blew everyone’s socks off. We went expecting a bit of juggling and firepoi, and were presented instead with a Wizard of Oz-style musical fireshow featuring Opiuo and an assortment of other psy-breaky joy. The kids practically wet themselves with excitement - we were worried for their eyebrows at one point. It helped that they were also bloody lovely people - such a great initiative - http://performerswithoutborders.org.uk. Many beers came after.

En route from the airport, Gora (my flatmate, fixer and all-round source of fun) nervously warned me that the apartment would be “basic”. However, my room is massive, opens on to the balcony and is quickly decorated with post-it notes. Pretty chuffed, really.

Developing an obsession with the yellow bumble-bee taxi cabs. The drivers are a mixed bag (as with anywhere in the world). There are various techniques you can use to persuade them to use the metre. About 1 in 3 will do so willingly, otherwise it’s bribery and flattery to avoid white-girl rates. Most are baffled when I ask to get where I’m going in Bengali. The others will generally succumb to the promise of “meter plus extra”

Arrival in Calcutta. There’s a balcony with a view of the street. This is where I have been doing all of my nervous chain-smoking since I got here. I practically have this sight burned into the back of my retinas by now.

I’m here volunteering on a three-month placement for the Hope Foundation, an Irish NGO dedicated to the protection of children from the streets or the city’s many slum communities.

So this is my quarter-life crisis: I packed in my perfectly great job, said goodbye to my home, family and friends in the UK and moved halfway across the world. The motivation was threefold: First, I love India, and I’m fed up with being just a tourist here. I want to spend time in the country and experience life beyond the backpacker circuit and temple trail. Second, I work in social design in the UK, and for a long time I’ve wanted to see if the service design methods I’ve been using in the public service sector could be applied in an NGO setting. Third: In London, I could see exactly how the next decade of my life would go. And sorry, but fuck that.

So here I am. No idea what the hell I’m doing; a beacon of blonde conspicuity. I’m terrified but never happier.

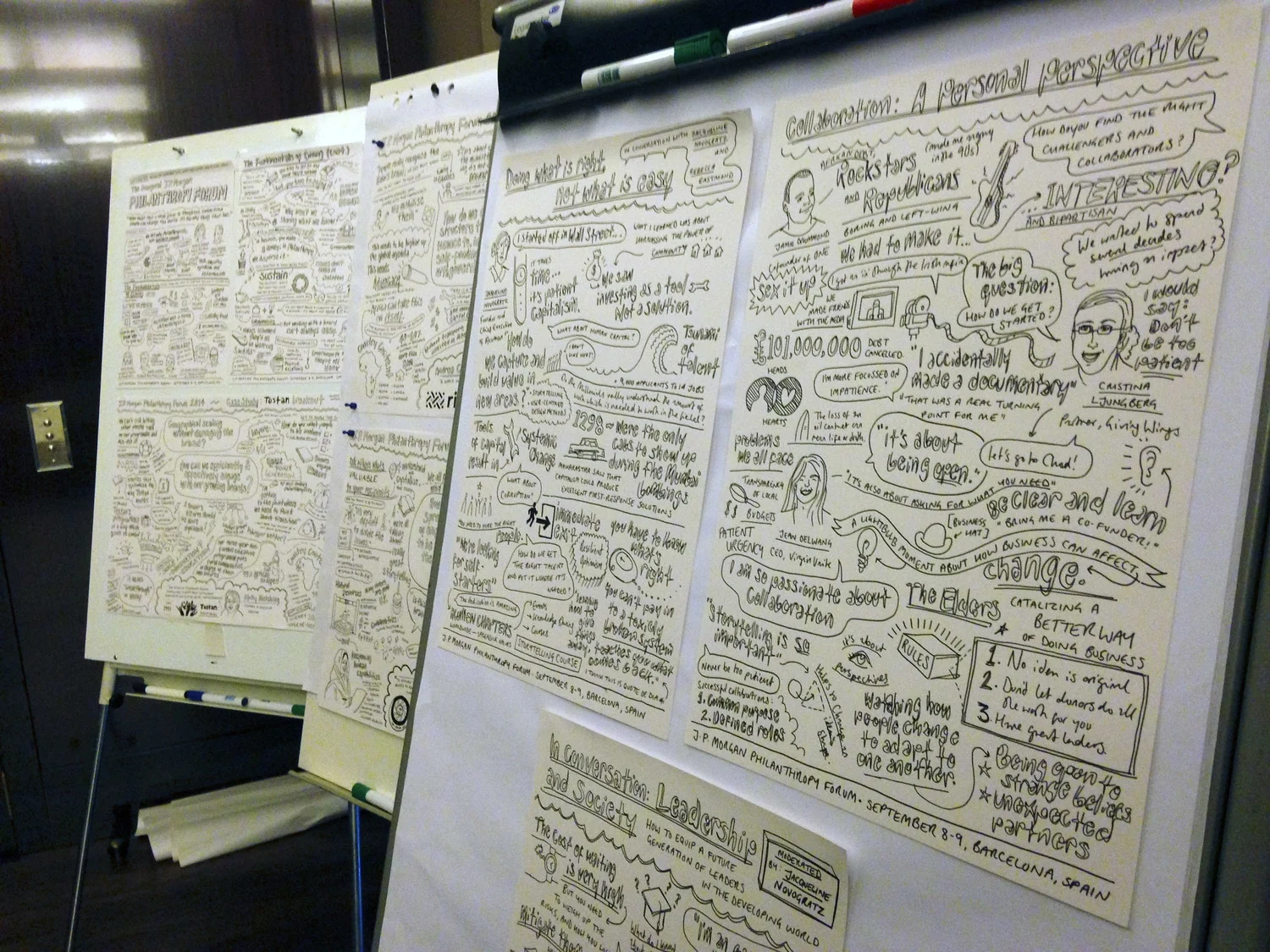

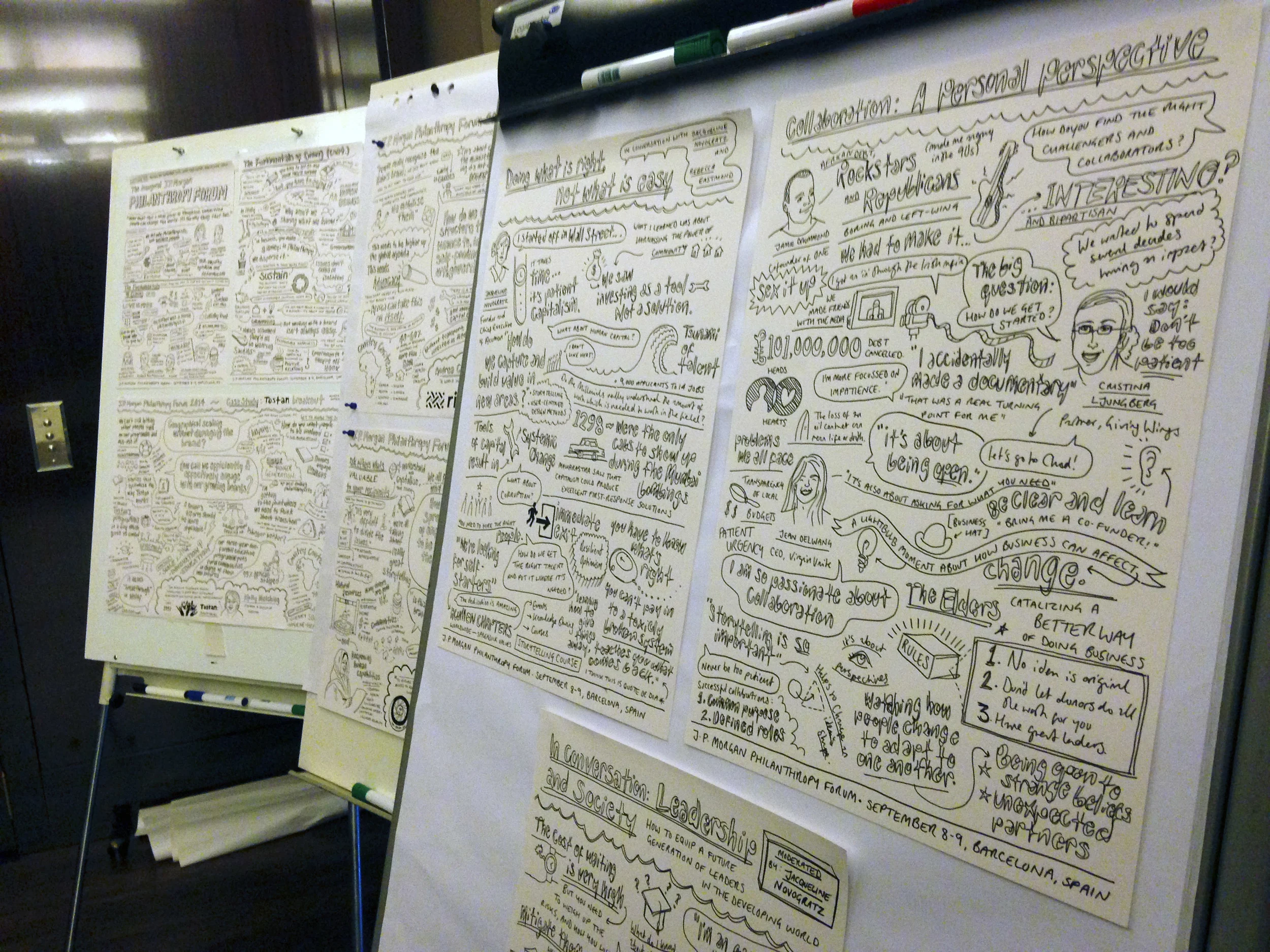

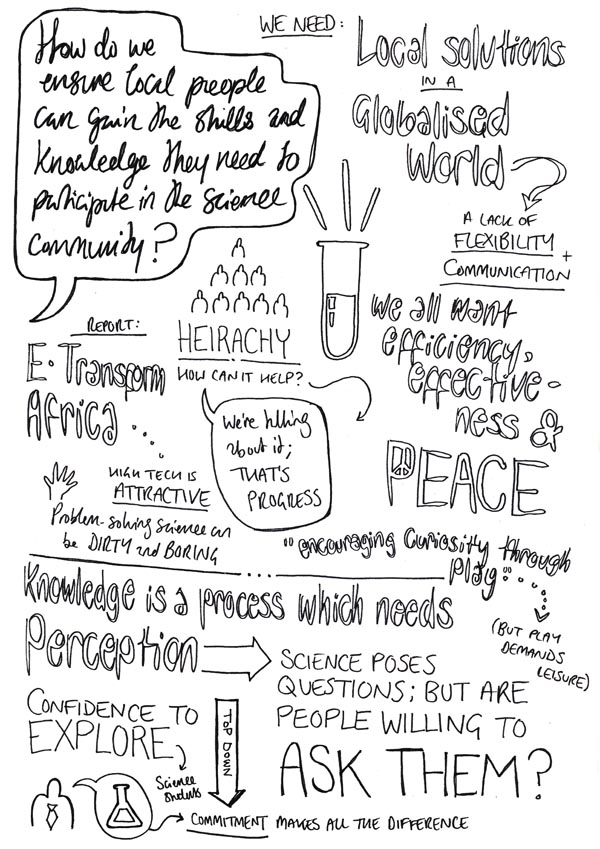

Sketchnotes at the International Philanthropy Forum, Barcelona

It almost seemed like a joke when I received a call from the world's most renowned private bank offering to pay me to fly to Barcelona and draw pictures of an exclusive and totally fascinating conference on development and philanthropy. It took all of about 5 seconds to consider my answer. The job was two intense, humid days of non-stop, limb-splintering concentration; a fly-on-the-wall insight into some of the world's most pressing and meaningful issues from a group of the world's cleverest, most influential and most inspiring people.

Bizarre, stressful, uplifting, frightening and at times outright exhilarating - I can't show more than snapshots of the work produced, but I'm damn well pleased that I could be there.

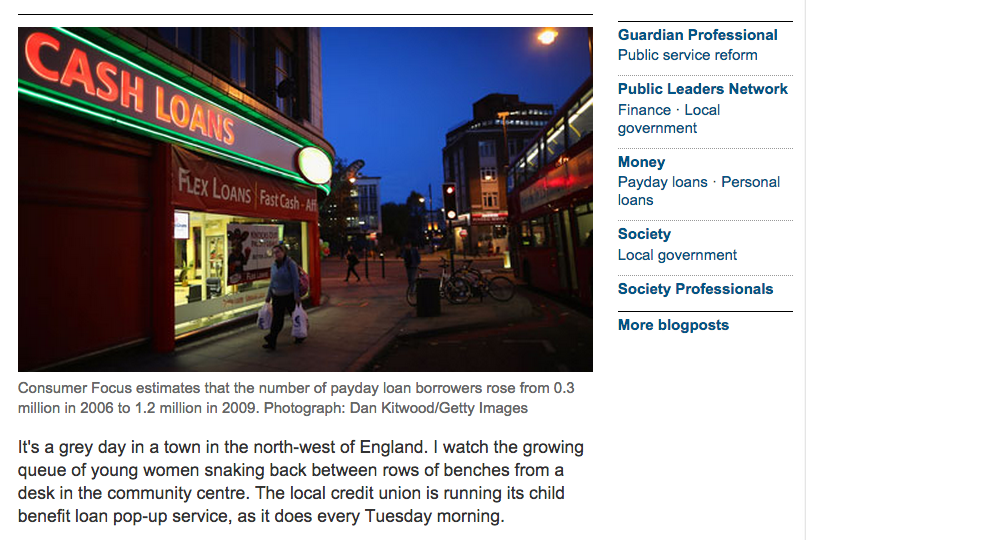

I wrote an article for the flippin' Guardian

I recently wrote a piece reflecting on debt culture, credit unions and payday loans for the Guardian. Informed by research into my latest project at FutureGov, Popcash - a money management tool to help financially vulnerable individuals stay on top of their personal banking and essential payments. Find out more about the project here. Read the original article here.

Payday loans: good financial behaviour lessons in school are the solution

High-interest loans have become an easy scapegoat, distracting attention from the issues around why people get into debt: these include late payment and overdraft charges – and avoidance

It's a grey day in a town in the north-west of England. I watch the growing queue of young women snaking back between rows of benches from a desk in the community centre. The local credit union is running its child benefit loan pop-up service, as it does every Tuesday morning.

I'm here to observe the union's processes, and to chat to its staff and members. I am in the midst of the design-research phase of FutureGov's latest project, Popcash.

The brief is to design a mobile product that enables credit unions to serve a 21st century clientele and compete with payday lenders such as Wonga by pointing people to more responsible sorts of loan, and building financial literacy and resilience.

I hope the app will be an alternative money-management tool to help people with their essential payments (and avoid incurring penalties or other charges, which can so often be the cause of a downward spiral).

The app works to signpost sources of help at the first signs of trouble, by encouraging the user to get in touch and build a relationship with their lender as soon as it sees they may have trouble keeping up with their payments. It will channel people towards organisations that can help with debt, as well as more responsible loan sources such as credit unions.

The incentive for creating this app is well documented: Consumer Focus estimates that the number of payday loan borrowers rose from 0.3 million in 2006 to 1.2 million in 2009 .

Our research study in Lewes, East Sussex, showed that payday and doorstep lenders now play a very real part in the daily lives of those living on the financial edge. Credit unions are often touted as a solution to the dangerous slide toward high-cost, short-term loan culture. As not-for-profit financial cooperatives owned by their members and run for their benefit, they are willing to offer low-interest loans to people who are likely to be refused credit elsewhere; the same people most likely to be tempted by the payday lender's promise of fast, anonymous credit with no or very few questions asked.

But as I watch Mary – the loans registrar – digging into her own purse to dole out her customer's withdrawals (it's been too busy to nip to the post office for more cash), I begin to question whether they can be solution to the payday loan dilemma, at least on their own.

Awareness and access are two issues vital for a credit union's success. Wonga seem to have an ad emblazoned across every second London bus at the moment (they spent over £16m on advertising in 2011) and deliver an average money-to-bank time of just five minutes. While credit unions are a diverse lot, not only is marketing at that scale a stretch, but from what we've seen they struggle to match the user experience the payday lenders provide; almost without exception they lack the infrastructure to support such speedy loans.

What's more, the APR cap of 26.8% means credit unions make a big loss on servicing small loan amounts: on a loan of £300 for one month they can only charge a maximum of just £6 interest.

The longer I spend around those in debt and those who work with them, the more I begin to question whether payday lenders are really the biggest problem. Time and again we heard stories of people whose debt problems have grown out of late payment and overdraft charges, which were the start of a downward spiral of managing interest repayments but never managing to pay off debt. This spiral is exacerbated by the typical response of avoidance. Step Change debt charity say that of 950 clients surveyed, more than 40% had struggled with mounting debts for a year or more before seeking help. We have heard of – and seen – several situations where carrier bags full of unopened letters are shoved behind the sofa.

Payday loans are undoubtedly a bad thing, but they have become something of an easy scapegoat distracting attention away from many larger critical issues around ethical practice and financial literacy. Broadly speaking, the solution is to teach better financial behaviour in schools. In the meantime, it's vital that existing council and independent advice services are clearly signposted and councils work to support their credit unions.

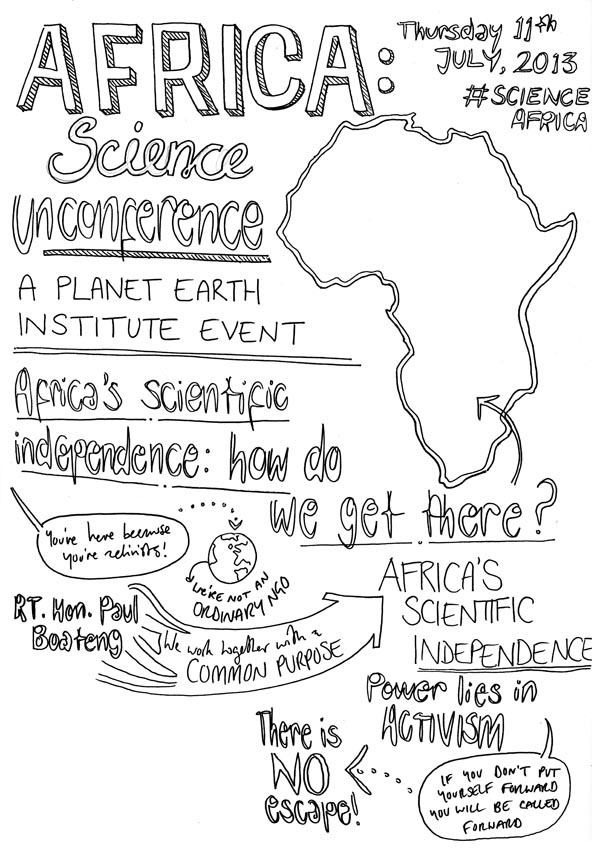

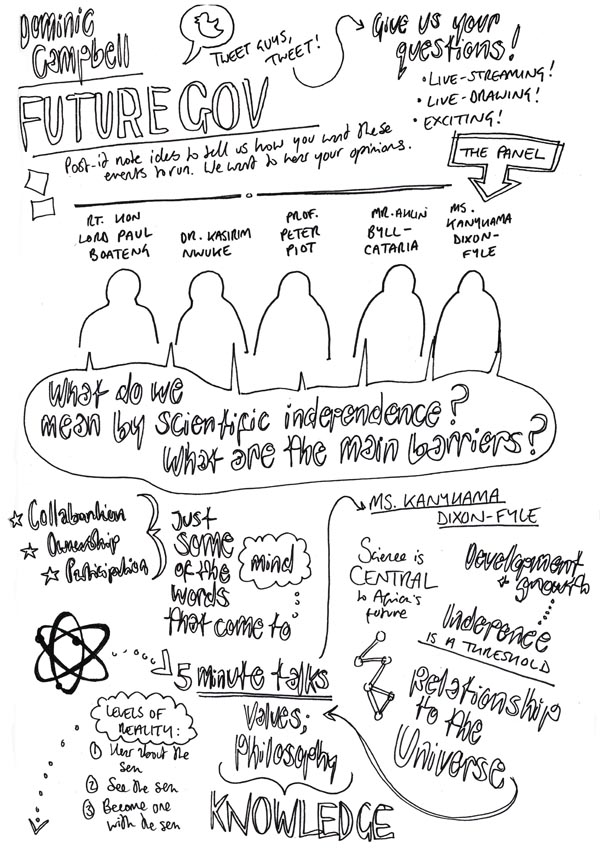

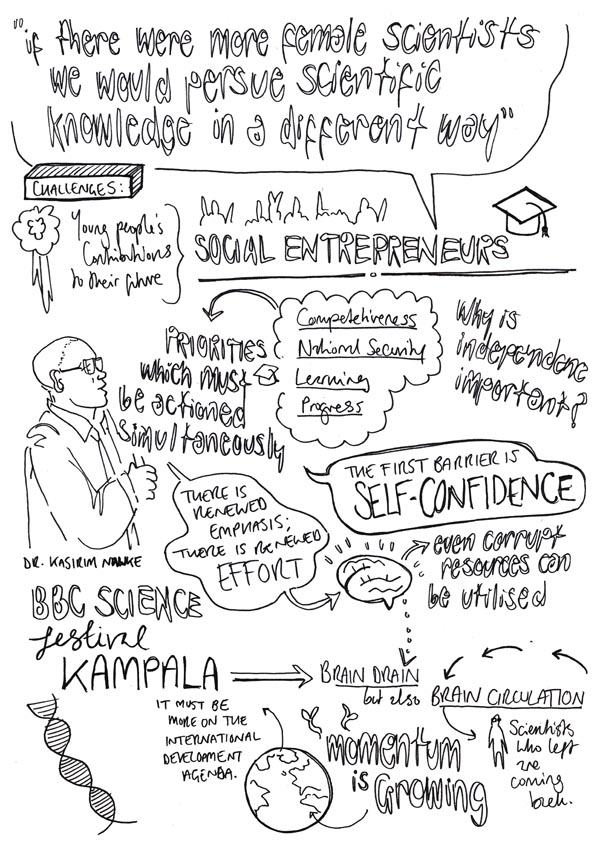

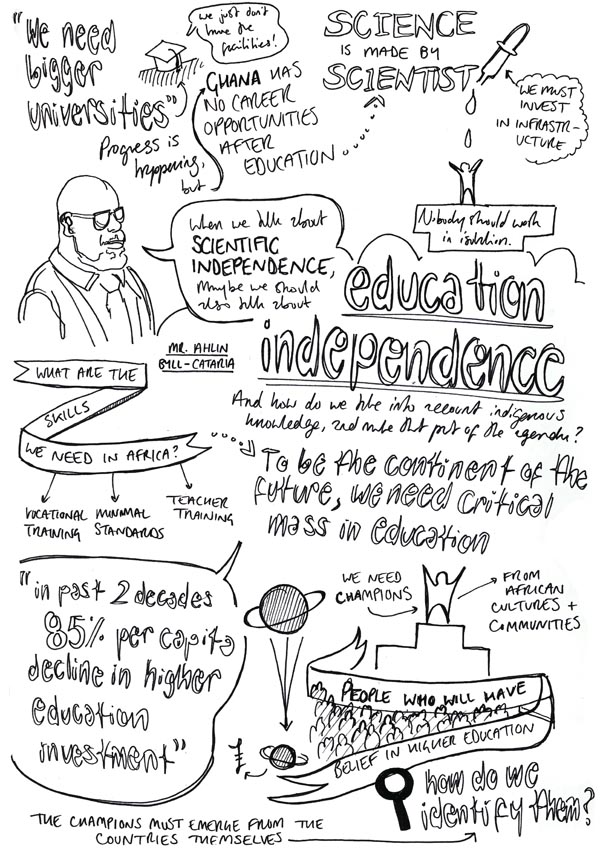

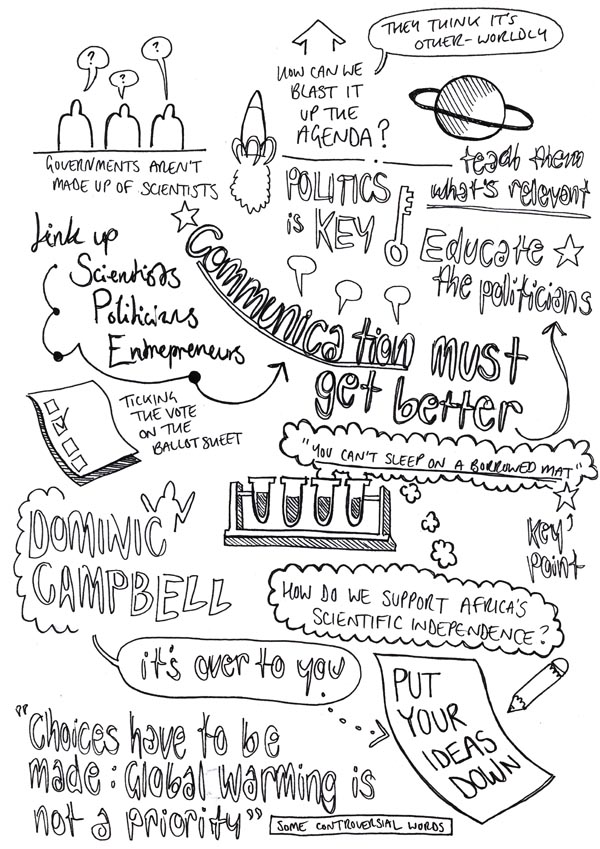

Science Africa Unconference

Last month I was asked to scribe at Planet Earth Institute's Science Africa Unconference. The Planet Earth Institute is an international NGO and charity working for the ‘scientific independence of Africa’. They build their work around three pillars, of higher education, technological innovation and advocacy and policy. FutureGov ran a Simpl challenge asking guests to suggest possible ways of making Africa more scientifically independent. The day was a huge success with talks, workshops and a darn incredible African lunch (it's all about cassava chips). Nice perk of the job.

Another Sunday Gif Activity

So I have been getting pretty obsessed with hand-drawn animation lately. Yesterday we deemed it far to cold to venture out of the flat, and spent much of the day browsing Vimeo's Staff Picks section. [You really have to check out this and this]

Now, it's not that I'm obsessed with tea or anything...

This is an hour's work using just pen, paper and iphone- then chucked into Photoshop. Now I'm imagining an entire day and what we could do with it.

Sometimes it's helpful when it rains.

Happy Mother's Day!

This whiled away at least an hour of Sunday afternoon. Happy Mother's day!

Wells Blog

Duis mollis, est non commodo luctus, nisi erat porttitor ligula, eget lacinia odio sem nec elit. Maecenas faucibus mollis interdum. Nulla vitae elit libero, a pharetra augue.